Trading or exchanging property has gone on for many years but there

were no clear IRS rules on how those transactions would be taxed.

That all changed in the summer of 1990 when the I.R.S. finally came

out with the long awaited rules on Deferred Exchanges. Section 1.1031

of the Internal Revenue Code laid out in detail the procedure for turning

a sale and purchase type transaction into an exchange. These new rules allowed the owners of business and investment Real Estate to buy and sell their property on the open market, and by following these simple rules defer the payment of the Capital Gains tax. The rules require that the property must be of “like kind” however the like kind provision for Real property is quite broad. It includes Land, Rental, and Business property. Any of which, can be exchanged for the other.

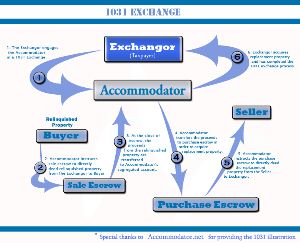

The rules also require that the "Exchanger" use a safe harbor to hold

the proceeds while the exchange was in progress, and spells out what those safe harbors are.

|